I spend a fair amount of time in Japan, and between the loyalty/point cards, train cards, and coins/cash, it's easy for your wallet (and pockets!) to become seriously bloated.

Here are a few tricks that I've picked up to keep things lean and minimal:

Load your loose change onto your transit card

Wallets sold here (and often elsewhere, too) typically have built-in coin storage, as these metallic denominations can be worth quite a bit. — In Japan, for example, they're up to ¥500, which is about $5 USD. Receiving these as change is quite common, and yet they're worth enough that it's a bit much to just toss them into a “loose change jar” at home and deal with them later.

… However, like most people, I hate carrying and counting-out coins at stores! There has to be a better way.

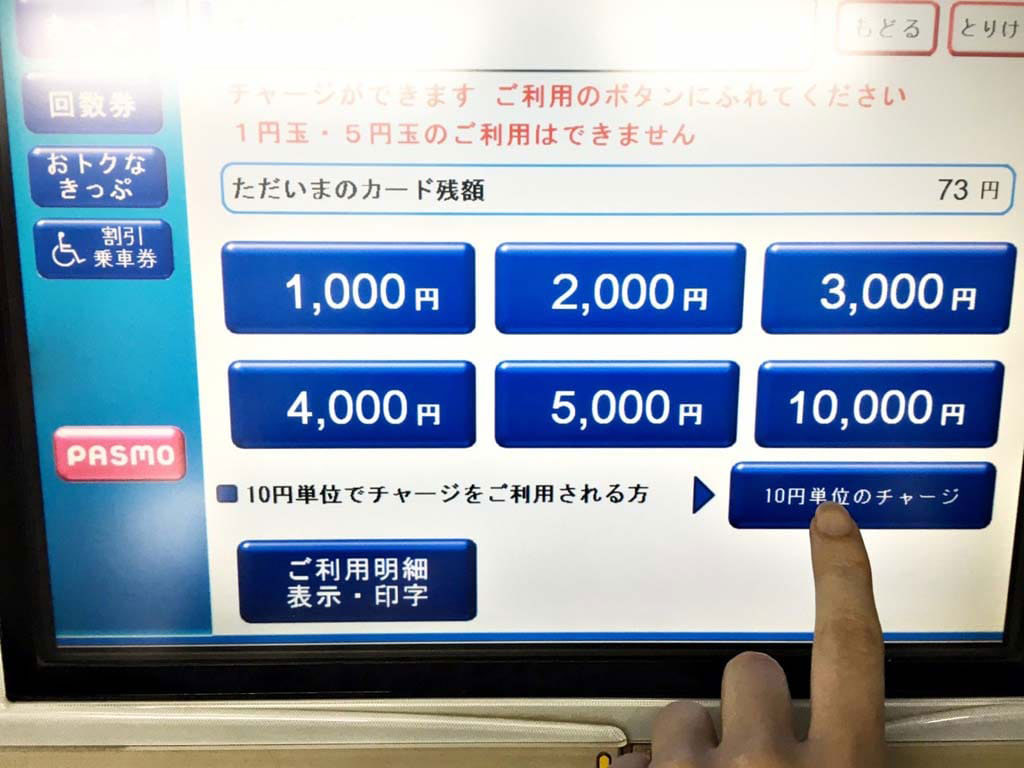

An under-appreciated feature of a significant number of the train ticket machines in Japan is their ability to load any multiple of ¥10 up to the maximum possible charge (depending on your remaining balance) onto your electronic transit card, which can then also be used for purchases at local convenience stores, vending machines, and some other places.

It's so quick/easy:

- Insert your Pasmo, Suica, or other supported FeliCa-type card into a non-JR ticket machine. (NOTE: JR machines only support charges in increments of ¥500, so you'll need to use the machines for the Tokyo Metro, or something else, instead.)

- Press the「10円…」button in the photo above, which is typically located just below the default suggested amounts. The interface for each machine can vary slightly, but will generally be of a similar format. — If you don't see this button, then that machine or train-line itself may not support small or variable charges.

- Then, dump all of your coins into the machine at once, and give it a few seconds to count them.

- Finally, type-in the displayed amount counted to charge your card with as much of what you inserted as possible, and you're done! Bye-bye extra coins.

With this trick, you can insert nearly all of your coins at once, have them counted, and afterward you'll only be left with the ¥1 and ¥5 ones.

Having only two different types of coins left over is way easier to manage, and since one of the two is bronze and the other is silver, you can easily separate them and simply carry between ¥7 and ¥13 of these (total, at once) with you to eventually get rid of them through everyday purchases.

Move your point cards onto your smartphone

Japan loves point and loyalty cards, and some of the more popular ones can be loaded into your smartphone through dedicated apps. This is nothing new, but a lot of these apps are still absolutely terrible. Slow to load, awful design/graphics, haven't been updated in years, etc.

Imagine visiting a store and trying to make a purchase, only to be presented with: a login screen, loading indicator, error message, or all of the above! — All of this, just to display a barcode? Come on. 😑

Some users have resorted to taking screenshots of the apps' barcodes in the past to avoid using the apps themselves, but there's a better way.

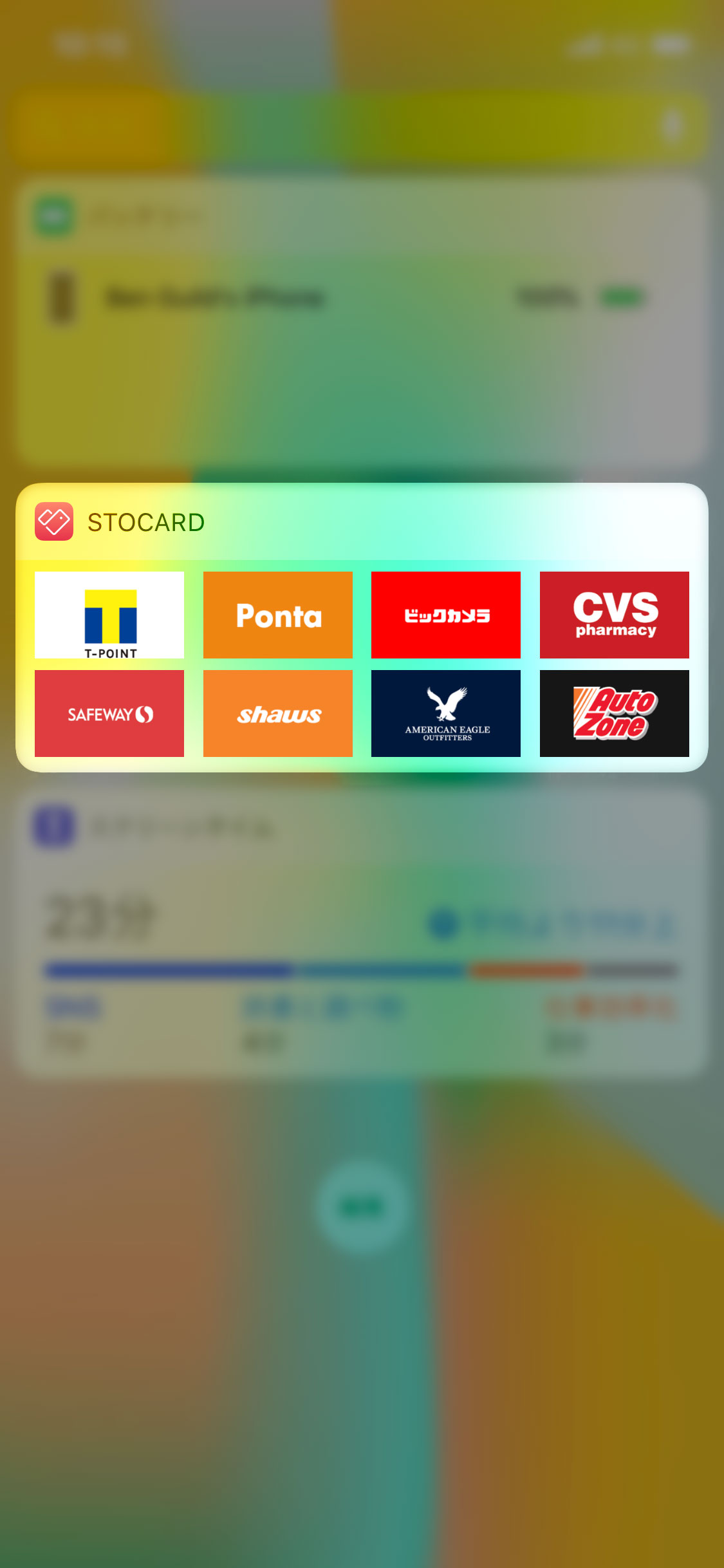

I like this app called Stocard that lets you create and quickly access digital versions of these cards from a “Today” screen widget on iOS, just by swiping-left on your device's homescreen! There's an Android version of the app, too.

Most of the point/loyalty cards that you have can probably be scanned into this app so that you don't have to go digging through your phone or wallet in order to earn points when checking out. — I generally only open the cards' own branded apps when I want to spend the points with a purchase or manage my account for one of them. It's so much faster and consistent to just use a single app/widget for this!

Unfortunately, Stocard doesn't yet let you “scan” a screenshot from your device's photo library (at least on iOS at this time of writing), but you can email or AirDrop one that you take to yourself and scan that screenshot off of your computer or another device, for example. — I recommend scanning your cards in rather than typing the numbers manually, as sometimes there can be trailing digits that are missing from the numeric label itself. Better to let the app do the work.

…If you've never taken a screenshot on your iPhone, just press either the power and home buttons at the same time, or the power and volume-up buttons at the same time, depending on which iPhone model you have! 📲

Carry the right credit card(s) and ditch the losers

One of the best ways to eliminate the need to hold onto most of your paper receipts while also avoiding ending up with a ton of cash or loose coins is to just use credit cards. I'd say most of the places I go on a regular basis now in Tokyo accept at least one of the two, if not both. However, if you don't have the best cards (or, if you have too many), you're leaving cash (or points) on the table that you otherwise could take advantage of, and this may offset the need to carry more point cards or cards with overlapping benefits.

Personally, I find Japanese credit cards to be way less competitive with the ones in the USA… many of which do not have a foreign-transaction fee and therefore have no real penalty when used abroad. — As long as the cards themselves don't [secretly] hide any additional costs for using them overseas or cross-border (such as in the exchange-rate itself without telling you upfront, or by applying a delayed or reduced exchange-rate in the bank's favor, etc.), there's not a huge disadvantage to getting the best card you qualify for from any country aside from the mild increase in complexity you may inherit in additional accounting cross-borders.

Just ask any card company if they have any foreign transaction-fees or exchange-rate adjustments like this.

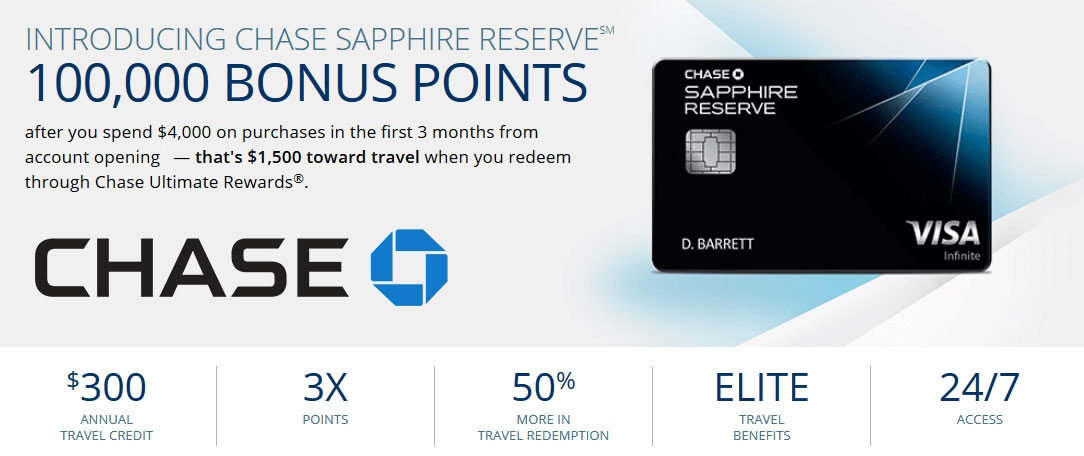

Chase Sapphire Reserve Card 👍🏻

A lot of people like this card, especially because of its generous sign-up bonus and 3X points rewarded on almost all travel and dining purchases, including things like Uber, airline tickets, and even coffee shops.

If you apply for this card, I'd of course appreciate it if you'd use my referral link! 😎

What's Hot:

- 3X points on almost all travel and dining purchases. What are these points worth? That's a 4.5% cashback equivalent when they're redeemed for travel rewards on Chase's website (such as flights and hotels), and 3.0% otherwise. Very nice. — For non-travel/dining purchases, it's only 1.5% and 1.0% respectively, so maybe use a different, more-targeted card for those purchases.

- Card is lightweight and discrete, yet made of metal.

- There's usually a sign-up bonus for this card that's worth at least several hundred USD in points.

- Even if you decide that you don't want this card in a year, you can downgrade the card to one of the Chase Freedom cards for free, which have no annual fee and can offer the same 1.5% cash-back on all categories… just without the 3X bonus on travel and dining, and other premium benefits. (While these Freedom-type cards do still have a foreign-transaction fee at this time of writing, you actually may still want to carry this card alongside your Chase Sapphire Reserve Card due to the optional 5% cash-back rotating bonus categories on one of the cards in particular. I wrote more about this in the “cards that I sort of like” section below.)

What's Not:

- $450 USD annual fee (at time of writing), but up to $300 USD per-year is instantly reimbursed back to you as a statement credit for any charges in the travel category… which as mentioned include public transit, taxis, Uber, airline tickets, and others. — If you don't think you'll earn at least $150 USD more back from the points and other benefits in a year, maybe start with one of the Chase Freedom cards instead.

- Apparently, the “purchase protection” benefit for lost or damaged goods on this card sucks compared to those on American Express cards, such as the American Express Platinum Card. This is what I've heard from a friend who's tried to use this benefit before with Chase and has cards from both companies.

As mentioned, if you apply for this card, I'd of course appreciate it if you'd use my referral link! 🙌🏻

Other cards that I sort of like, but might cancel

I've had a few others in the past which I don't really use anymore, but they might be a good fit for you.

- American Express Platinum Card: Personally, if you don't stay in chain hotels often, the only strong benefits of this card in my eyes are its reliability, its complimentary access to the AMEX Centurion lounges at certain airports with hot-food and spas, and its notably good “purchase protection” in case of something getting lost or damaged within 120 days of purchase. If this is worth $550/year for the annual fee to you, then go for it, but otherwise the cashback-rate equivalent with the points on this card is more like 1% if you don't factor in the other benefits. — For Japan, it is often good to have some sort of AMEX card if you don't have a separate Japanese credit card, because a lot of e-commerce websites and apps will otherwise automatically block all of your transactions. AMEX is an exception to this, as their cards are accepted seemingly universally… as long as it's at a merchant that accepts AMEX, though.

- Various 1.5% to 2% cashback cards (including the Chase Freedom Card): There are a lot of these and they're all similar with few exceptions, but they pretty much all offer a fixed cashback-rate on all purchases in any purchase category. Almost always, these cards have at least a 1% foreign-transaction fee. This essentially makes any of the other cards that I've primarily mentioned a probable better choice when shopping overseas… except for in the case of the rotating bonus categories on the plain Chase Freedom card. This card in particular largely offsets its own foreign-transaction fee if the points are then transferred back to the Chase Sapphire Reserve Card for a 1.5X bonus. (…effectively earning an astounding 7.5% cash-back, which is ≈ at least a 4.5% peak cash-back rate for that card when you factor in the possibly applicable 3% foreign transaction-fee.)

I will also say that I've had some quality concerns with the American Express Platinum Card, as its two adhered sheets of metal tend to separate over time, as shown here:

This multi-layer separation issue is not a problem on the Chase Sapphire Reserve Card, as it's a single layer of metal and therefore also slimmer and more lightweight.

Scan your receipts (and other paper) then get rid of it

With convenient cellphone cameras and powerful/smart scanning apps, as well as high-quality desktop document scanners, lingering paper is more quickly becoming a thing of the past.

By digitizing your receipts into a notebook inside Evernote or Bear, for example, you can avoid accumulating collections of paper while simultaneously having it be text searchable. You have to keep some records in the case you need to exchange/return something and/or eventually file claim on your credit card for purchase protection, extended warranty, or item loss, so maybe do this to avoid having to keep the paper around for too long.

You can use the document scanners built-into the note-keeping apps that I mentioned above, a high-quality desktop physical scanner for partial bulk automation, or even a standalone app such as Evernote's Scannable app.

Tip: If you don't want to keep your stuff “in the cloud,” maybe go with the desktop scanner and scan into an app on your computer instead of using a mobile-app.

Enhanced searchability

Depending on which software you use to store the scanned documents, sometimes its search technology can recognize text within the scanned images using optical character-recognition (OCR) and locate text within the scanned documents by keyword or contents, which can be great for looking stuff up from a while back.

I believe with Evernote in particular this is limited to those who are premium subscribers, but you can also alternatively add your own tags or text descriptions to the notes themselves and do something similar manually.

Move your transit card(s) onto your smartphone

If you live in Japan, you've probably heard of this already, but if you have an iPhone 8, iPhone X, or newer (or an iPhone 7 if it was bought in Japan), you can convert your Suica card to instead be a “Mobile Suica” on your device. — A few Android phones in Japan have also supported this in years past, but support overall will hopefully increase significantly over the next few years as Google ramps up its Google Pay service.

Advantages:

- No need to carry the card with you anymore… just your phone!

- You don't need to unlock your phone to use it. You can just tap it on the reader anywhere. — This is different from other Apple Pay implementations, as Suica cards have two-way communication and the card is programmed to only allow storing a balance of up to ¥20,000. (approximately $200 USD)

- Instant refund of the deposit you made when receiving the card initially. (+¥500 bonus!)

- You'll be able to charge your card's balance with any of the credit cards that you have linked to your device with Apple Pay!

Mild disadvantages:

- Depending on whether you're left or right-handed, and which pocket you typically keep your phone in, you may need to adjust your habits since all of the payment pads are typically on the right-side as you enter train stations. — This especially goes for left-handed people who want to use this feature from their Apple Watch.

- If your Suica has your name written on it (a “MySuica” card), and your name is not written in Japanese (it's using the Latin alphabet, ローマ字), you'll need to visit a JR ticket office and ask them to convert it to be written in Katakana before this will work.

- Since this is a hardware-based solution, this is even usable while your phone is rebooting. However, if your phone's battery dies while you're on the train, you'll have to ask for a note from the staff when trying to leave the station.

- If you want to change devices (for example, if you bought a new phone), apparently you need to manually remove the Suica card from your old device before adding it to the new one. I haven't tried this yet, but just keep it in mind. I've heard that the card will be suggested as being “addable” on the new device automatically as long as it's not still active on another device and as long as you're logged-in with the same Apple ID, but I have yet to confirm.

- Non-JR ticket machines (at this time of writing) do not support charging physical devices, only plastic cards, so you'll have to charge using a credit card. — Furthermore, while some of the JR machines do support both physical devices and plastic cards, none of these newer machines currently (and probably ever) will accept coins… only cash. Therefore, you won't be able to load your loose coins onto your Mobile Suica until or unless either of these limitations happens to be alleviated. 😕

Overall, I'd say go for it if your device supports it. 👍🏻 — To move your physical Suica card to your digital Apple Wallet, temporarily set your device region to Japan if it isn't that already (you can change it back after), and then follow the steps shown here!

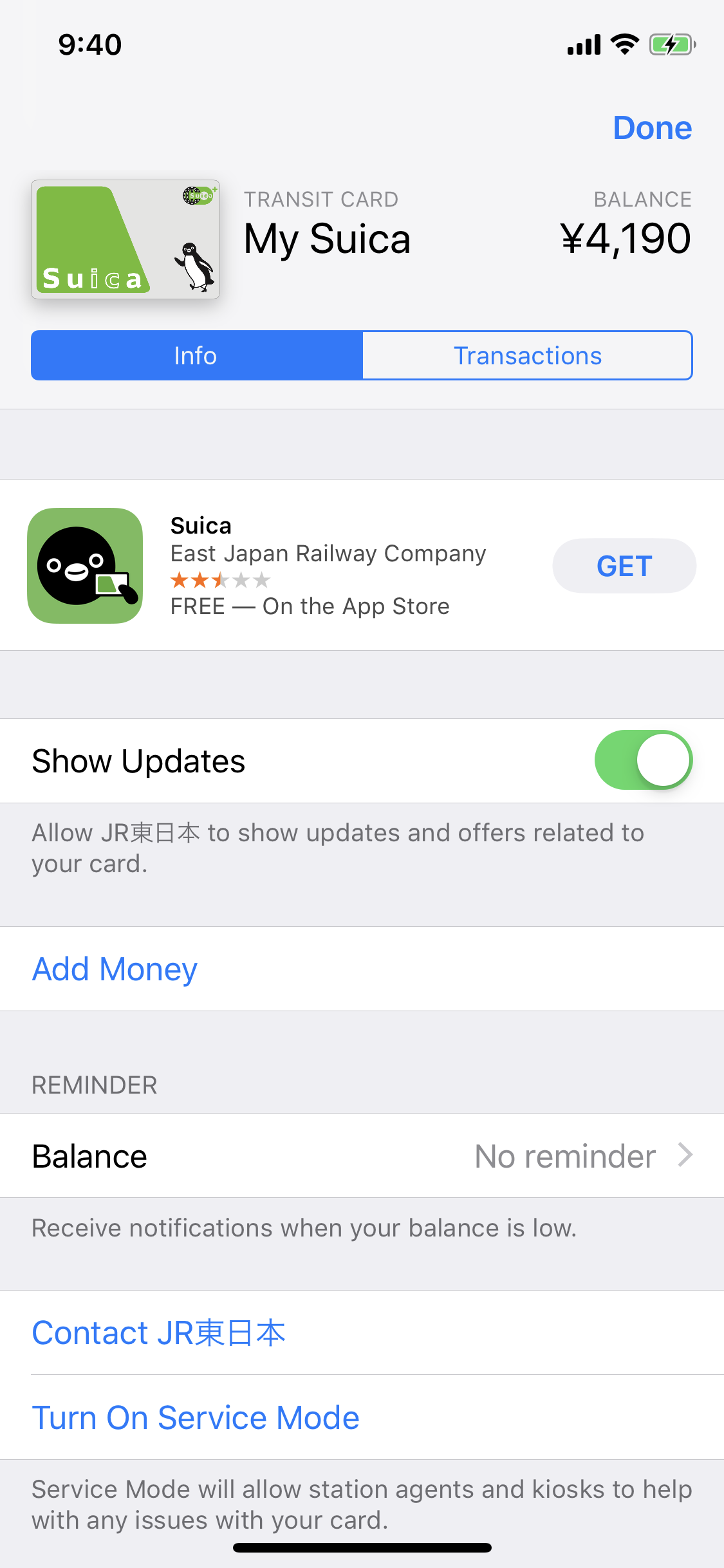

Bonus Tip: You don't need the Suica app!

It's worth mentioning that you don't actually need to have the Suica app installed on your device, ever. For some reason, this is not well understood.

The easiest way to charge and manage your Suica is just by using the Wallet app that comes pre-installed on your Apple device:

- Open the “Wallet” app from your homescreen.

- Tap on your Suica card in the list of cards.

- Tap the round ellipsis/info button shown in the bottom-right corner, and you should see the same screen shown above… listing your balance and other options. — One of these options is to “Charge” the card using any supported credit or debit card that's already linked to your device with Apple Pay.

If you have the Suica app installed and this works better for you, you can safely delete it and you won't lose access to charging this way.

Conclusion

All you really need these days is a few physical cards, a bit of cash (if you need cash), and maybe some loose change kept in a spare pocket. Generally, in the USA nowadays, I don't even carry cash at all. — These tips in general can hopefully help you avoid carrying too much of anything mentioned. (YMMV, depending where you are!)

Don't let your wallet or bag end up like George's! 😄